The Difference Between a Tax Credit and a Tax Deduction

Saving money is on a lot of Americans' minds as April approaches. You may have heard that you can lower the amount of taxes you owe with tax deductions and/or tax credits, but don’t know the difference between the two.

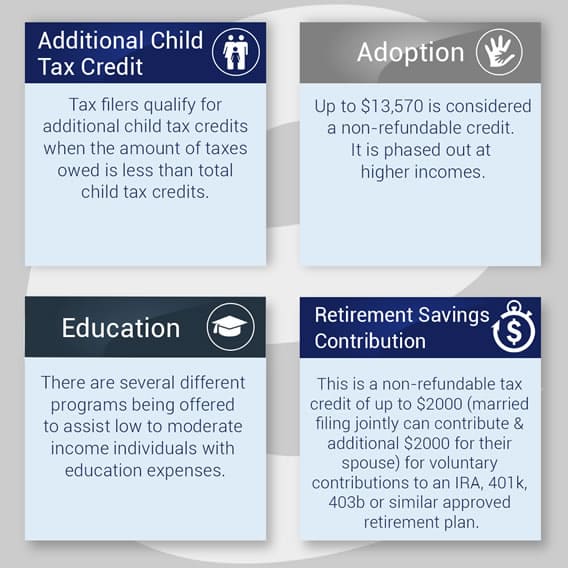

Tax Credits

Tax credits lessen your tax burden dollar-for-dollar, so the math is simple. As of 2020 , the IRS lists at least 14 tax credits available to individual tax filers, as well as multiple deductions in the following categories:

- Education

- Homeownership

- Health care

- Savings and income

- Family and dependents

So when you do your taxes, let’s say you take $1,000 of the Lifetime Learning Tax Credit (a tax credit for tuition and enrollment fees should you, your spouse, or a dependent pursue education at a qualifying college or university) and you owe $2,000 in taxes. The tax credit reduces your tax bill by $1,000, so you end up owing the IRS $1,000. If you qualified to take the full $2,000 tax credit, you would owe $0 in taxes.

In most cases, tax credits are non-refundable, meaning they can reduce the amount of tax you owe to $0 but can’t result in a refund. There are a few tax credits that do result in a refund, however. Tax filers also should be aware that not all tax credits are for all tax filers. Some of them have income limits and other qualifying standards, such as age, filing status, employment, and education. Read more on IRS tax credits

Tax Deductions

Tax deductions lessen your taxable income based on your marginal tax bracket so you get some benefit. You don’t save as much money with a tax deduction as you do with a tax credit. The IRS offers tax deductions to individuals in several categories, including job-related, business-related, investments, and healthcare deductions. If you qualify for a $1,000 tax deduction and you’re in the 22% tax bracket, that means you can deduct $220 from your taxable income.

Most people take tax deductions, and the standard and itemized deductions are the most common. You might take the standard deduction—an amount set by the IRS—if you don’t want to itemize your deductions, or if your itemized deductions add up to less than the standard deduction. The IRS bases the standard deduction on whether the taxpayer is 65 or older and/or blind and whether another taxpayer can claim them as a dependent. You might itemize your deductions if they add up to more than the standard deduction. Read more on federal tax deductions

Below is a short quiz to test your knowledge on the subject of tax deductions and tax credits.