Types of IRS Tax Forms: A Reference Guide

Understanding the different types of tax forms is the first step to filing with confidence. IRS tax forms generally fall into a few broad categories: individual income tax returns, informational returns, supporting schedules, and business tax forms. Knowing which category applies to your situation is the fastest way to identify what you need to file.

Below is a reference guide covering some of the most common IRS tax forms that you are likely to encounter. While the IRS publishes hundreds of forms, this guide focuses on the types of tax forms that come up in everyday tax situations, along with a brief explanation of when you’d use them.

If you’re filing for the first time, you’ll most likely need your W-2 or 1099-NEC from your employer, a Form 1040 to report your income, and any supporting schedules that apply to your deductions or credits. Not sure which of these forms applies to you? See what documents you may need to file your taxes.

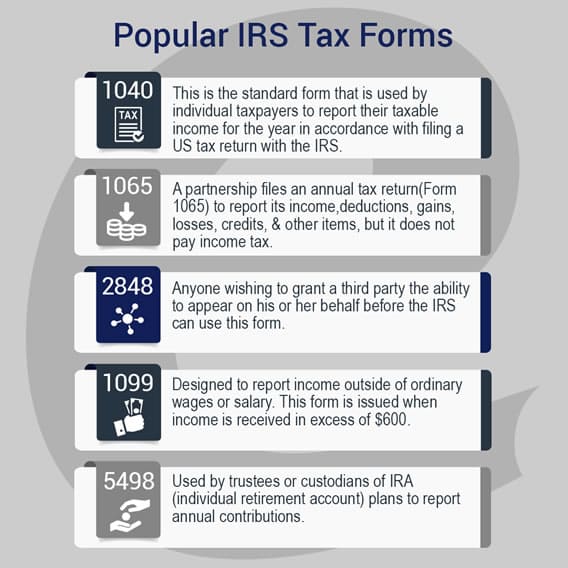

1040

This is the standard form that is used by individual taxpayers to report their taxable income for the year in accordance with filing a US tax return with the IRS. Requires information on income, usually in the form of W-2 and 1099 earnings but also dividends/interest, capital gains, and retirement distributions. Any deductions claimed or credits earned may also be reported on this document.

The 1040 is supported by three numbered schedules, which are filed alongside the 1040 when applicable. Schedule 1 for additional income and adjustments, Schedule 2 for additional taxes, and Schedule 3 for additional credits and payments.

Note that the 1040-SR is a version of the standard 1040 designed specifically for taxpayers age 65 and older, featuring larger print and a built-in standard deduction chart, but it is otherwise identical in what it reports.

1040NR

To be used by non-resident (alien) individual taxpayers when filing a US tax return. Those non-residents who worked/earned wages in the US or students who received grants, scholarships, stipends or allowances for attending school in the US will likely need to file a NR.

1040X

Designed to serve as an amendment to a previously filed tax return. Used to correct errors or make adjustments to taxpayer 1040, 1040A, 1040EZ, 1040NR or 1040NR-EZ documents.

1040-ES

Form used to accompany individual estimated tax payments made to the IRS. This is one of the most important obligations for self-employed individuals and freelancers. ES payments are made on a quarterly basis and due on April 15, July 15, September 15 and January 15 (with the exception of years where the 15 falls on a Saturday or Sunday in which case they are due the following Monday). Depending upon the amount owed on the prior year’s tax return, estimated payments may be a requirement for the individual.

1041

Used to file the income tax return for an estate or trust. Reports information such as income, deductions, liabilities, gains, losses, employment taxes and other data for the estate or trust. Must be used if the gross income is $600 or greater or if it has any taxable income, even if it is less than $600. Also, it must be used if a non-resident alien is the designated beneficiary.

1065

A partnership files an annual tax return (Form 1065) to report its income, deductions, gains, losses, credits, and other items, but it does not pay income tax. Instead, it passes profits and losses through to its partners on Schedule K-1. Copies of Schedule K-1 are sent to the partners and a copy is filed with the IRS. Each partner then includes his or her share of the partnership’s items on his or her own return.

1098

This is for individuals who paid more than $600 in mortgage interest during a tax year. The company servicing the mortgage issues it. The form includes information about prepaid interest points, the amount of interest paid during the prior year and sometimes-additional information. Although corporations, partnerships and most other types of businesses do not have to file this form for mortgage interest, a sole proprietor must use a 1098.

1099

Designed to report income outside of ordinary wages or salary. This form is issued when income is received in excess of $600. All income reported on a 1099 should be included on the taxpayer’s US tax return. Variations of this form are available for many things such as sale proceeds, dividends, interest payments, contractor services and even retirement distributions.

Common variants include the 1099-NEC (freelance and contractor income), 1099-MISC (miscellaneous income), 1099-R (retirement distributions), 1099-INT (interest income), 1099-DIV (dividends), and SSA-1099 (Social Security benefits).

1099-NEC

The dedicated form for reporting payments made to freelancers, independent contractors, and other self-employed individuals. Businesses must issue a 1099-NEC to any non-employee they paid $600 or more during the tax year. The income reported on it must be included on federal tax returns and is also subject to self-employment tax.

14039

Form to inform the IRS that a person has become a victim of identity theft, and a Social Security number has been compromised. This theft affidavit alerts the IRS that current and future tax returns may be compromised so that a specific account can be marked to review activity.

2848

Anyone wishing to grant a third party the ability to appear on his or her behalf before the IRS can use this form. It serves as a power of attorney/representative. Up to three people can be appointed on behalf of a taxpayer who can also use this to revoke the power of a previously appointed representative. All selected representatives must sign the form before filling.

4506-T

This is a request for a transcript of a tax return. It is often used to evaluate and verify a person’s creditworthiness, especially when applying for a mortgage. It certifies that the claimed income on a loan application matches the income on a tax return. In other words, this is used as quality control by financial institutions to prevent loans from being issued based on inaccurate information.

4868

This is an application for a six-month extension to file an individual tax return. Must be filed by the April 15th tax deadline and should include the total estimated tax liability. This form does not extend the time a person has to pay his or her taxes just the filing of the return.

5329

The law limits the amount of money that can be contributed and withdrawn from tax deferred accounts and certain tax advantaged accounts. This should be filed whenever a person contributes too much money, withdraws too little/much, or withdraws funds for a purpose that does not conform to the type of plan (e.g. retirement, medical bills, etc).

5498

Used by trustees or custodians of IRA (individual retirement account) plans and various MSA and HAS plans to report annual contributions. Plan participants will receive this form from the plan by May 31 of the tax year following the contribution. The custodian also files the form with the IRS, so the plan participant simply needs to retain this copy for future verification if needed.

5695

Used to claim government-issued energy tax credits. Such as energy efficient windows, doors, insulation, roofing as well as Energy Star appliances. The form must include the costs associated with the improvements, installation dates, etc.

8283

Individuals who gave more than $500 in non-cash charitable contributions during the tax year must use this to report information about these donations. This includes donated vehicles, household goods and other items.

8332

This is used by a parent who is filing their taxes separately from the custodial parent. This releases them from the right to claim the dependent(s) on their tax return. The form is attached to the non-custodial parent’s tax return. With this you can designate the years in which the taxpayer is releasing their claim to this exemption. It can also be used to revoke a previously released right to claim.

8606

Reports nondeductible IRA (individual retirement account) contributions and conversions from a traditional IRA to a Roth. It is also used to report distributions from traditional, SIMPLE, or SEP IRAs if there have ever been nondeductible contributions made.

8821

A taxpayer can use this form to instruct the IRS that a lender or other entity is able to access specified tax-related documents. This filing includes the name of the organization being authorized to receive this information, its address, and the tax information that is being released.

8822

A taxpayer change or address form. Needs to be filled out and submitted any time there is a change to a home address. Should be transmitted to the IRS prior to receiving an anticipated refund check or critical correspondence.

8863

Used to calculate and claim the American Opportunity and Lifetime Learning tax credits for qualified education expenses. The attending college/university should send a 1098-T each year to anyone who pays tuition; this can be used to complete the 8863 accurately.

8879

The authorization required for a taxpayer’s electronic return to be filed through a tax preparer (electronic return originator). This is necessary whenever permission is given to generate a filing PIN or transmit IRS tax forms electronically.

8880

A credit for contributions to qualified retirement savings vehicles. This is used by taxpayers to reduce the amount of income tax they owe based on contributions to a qualified retirement plan. To complete this for a particular tax year, taxpayers will need to know how much they and their spouses contributed to an IRA, 401 (k) or 403 (b) plan via elective deferral, as well as the distributions they received from one of the aforementioned plans during the year.

8889

Used to report contributions to HSAs (health savings accounts). Anyone who made contributions to their plan or received employer contributions and wishes to deduct these from his or her income taxes must complete this form. Anyone who receives distributions from their plan or inherits an HSA, as a beneficiary after the death of the account holder, must also file.

8949

To be completed when reporting capital gains or losses on one’s tax return. Reports income from gains as well as capital losses so that the correct tax is paid/deduction taken. With this it is important to identify the date of acquisition as well as sales date to determine if the transaction is a long-term or short-term gain/loss.

Note that cryptocurrency is treated as property by the IRS, meaning any sale, exchange, or disposal of crypto must be reported as a capital gain or loss on Form 8949 and summarized on Schedule D.

8962

To be filed with an income tax return in order to determine the premium tax credit that may be due for the purchase of a qualified health insurance plan. To qualify for the credit, taxpayers must have a modified adjusted gross income that falls within a certain range and must not be eligible for employer-sponsored health insurance.

9465

This is an installment agreement request. It is used to ask the IRS to set up a monthly installment plan when a person is not able to submit the full amount of taxes owed. This form may be filed electronically with a tax return or filed separately using this form. It is important to note that the IRS does impose fees for using this type of agreement and charges interest for all balances not paid in full by their respective due date.

Schedule A

Used for itemized deductions. An individual taxpayer can either use the standard deduction or itemize deductions. Expenses qualifying as itemized deductions include unreimbursed medical and dental expenses, mortgage interest, state and local taxes paid, and charitable donations.

Schedule B

Interest and ordinary dividends are reported on this schedule if the taxpayer had over $1,500 of taxable interest or ordinary dividends and in a number of other situations, such as having accrued interest from a bond or reporting original issue discount in an amount less than the amount shown on Form 1099-OID.

Schedule C

A taxpayer uses this schedule to report income or loss from a business in which the taxpayer operated as a sole proprietor. A single-member LLC typically files Schedule C with a personal 1040. It is also used for:

- Wages and expenses the taxpayer had as a statutory employee

- Income and deductions of certain qualified joint ventures

- Certain income shown on Form 1099-MISC

Schedule D

A Schedule D form should be used to report capital gains and losses, specifically:

- The sale or exchange of a capital asset not reported on another form or schedule

- Gains from involuntary conversions (other than from casualty or theft) of capital assets not held for business or profit

- Capital gain distributions not reported directly on Form 1040

- Nonbusiness bad debts

Schedule E

A taxpayer should use to report income or loss from rental real estate (rental income), royalties, partnerships, S corporations, estates, trusts, and residual interests in Real Estate Mortgage Investment Conduits (REMICs).

Schedule EIC

Used to provide the IRS with the taxpayer’s “qualifying child” information if the taxpayer is claiming the earned income credit. The schedule is completed only if the taxpayer has a qualifying child.

Schedule F

Used to report farm income and expenses.

Schedule K-1

Used by Partnerships and S Corporations that pass income and deductions on to their partners or shareholders rather than paying/claiming them by the entity. Each partner or shareholder then pays/claims their share of the entity’s income and deductions on their own return.

Schedule SE

A taxpayer uses this schedule to determine the tax due on net earnings from self-employment.

SS-5

This is the application for a Social Security card. The same form is used whether the applicant is applying for a replacement card, changing or correcting information (such as a name change), or receiving a card for the first time. This can be completed online through the Administration’s website, or using this form.

W-2

A W-2 is an IRS form known as the Wage and Tax Statement. It is used to report wages and the federal income taxes withheld from those wages from the previous year to both the employee and the IRS. The employer is required to mail the form to each employee at the end of the year. The employee uses that form to report income to the IRS for tax purposes.

If you are missing your W-2 form, there are two ways to receive another copy. First, contact the employer that issued or should have issued a W-2 to you, and request another copy of the form. If they are unable to provide it, you must contact the IRS directly to get a copy of your form. You will need to provide information such as the name of your employer, your Social Security number, your contact information and other facts that the IRS requests. Note that if you do not receive your form, you are not exempt from filing a tax return for the year in question.

Employers use Form 941 to report wages paid and federal income, Social Security, and Medicare taxes withheld from employees each quarter.

W-4

Also known as the Employee’s Withholding Certificate, a W-4 is an IRS tax form individuals fill out when they begin work with a company. This form is used by employees to let their employer know how much income tax should be withheld from their paycheck each pay period. Employees must fill out a W-4 form to initiate tax withholding or to change the amount of pay they want withheld each period. Employees indicate the amount they withheld by stating their tax exemptions, a dollar amount they want withheld or a combination of the two.

W-9

This form is a request for a taxpayer identification number, either as a Social Security number or an employer identification number. This is typically provided by businesses to contractors so that the business may file the appropriate tax documentation (e.g., 1099) at the end of the year. It consists of the taxpayer’s name, address, identification number and signature.

Additional IRS Tax Forms and Resources

This guide covers the IRS tax forms most individual and first-time filers are likely to encounter, but with hundreds of forms in existence, it represents just a fraction of what the IRS publishes. For a complete list, visit the IRS Forms and Instructions library directly, or simply access the forms relevant to your situation automatically through tax filing software like E-file.com

Have more questions about filing? Visit our Tax Filing FAQ for answers to the most common tax questions.

Ready to file? Start your return on E-file.com

Frequently Asked Questions

What are the most common IRS tax forms?

The most common IRS tax forms include the 1040 (individual income tax return), W-2 (wages from an employer), 1099 (non-wage income), and Schedule A (itemized deductions).

What tax forms do self-employed individuals need?

Self-employed individuals typically file a 1040 with Schedule C to report business income, along with Schedule SE for self-employment tax, and may also need to file 1099s for any contractors they paid.

What tax forms do small business owners with employees need?

Small business owners with employees generally need Form 941 for quarterly payroll taxes, W-2s for each employee, and Schedule C or a separate business return, depending on their entity type.

What tax forms do retirees receiving Social Security need?

Retirees typically receive a 1099-R for retirement distributions and an SSA-1099 for Social Security benefits, both of which are reported on Form 1040.

What is the difference between a tax form and a tax return?

A tax form is any IRS document used to report financial information. A tax return specifically refers to the forms submitted to report income and calculate what you owe or will be refunded — most commonly Form 1040.

How do I get copies of IRS tax forms?

You can download current and prior year IRS tax forms directly from IRS.gov, or access them through tax filing software like E-file.com, which automatically provides the correct forms based on your situation.