IRS Payment Plans and IRS Installment Agreement

Stressed about how to pay the IRS? Fortunately, there are many ways to pay federal taxes, including IRS installment payments. There may even be a way to pay less than you owe or temporarily delay payments until you are able to afford them.

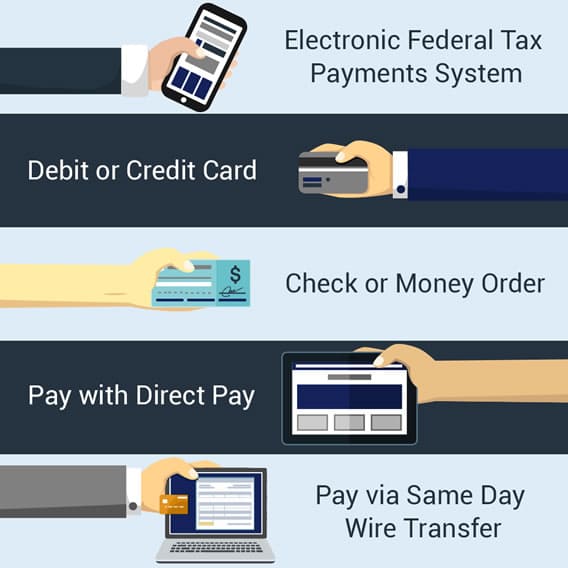

Ways to Pay the IRS (Internal Revenue Service)

There are more personal checks written to the US Treasury on April 15th than nearly any other day during the calendar year. With that said, fewer checks are being written than once were. This is in part because consumers have more options to pay their bills than ever before. This is true everywhere, but especially so at the US Treasury. Below you can find a list of the current approved payment methods for ways of paying your taxes:

- Electronic Federal Tax Payments System (EFTPS®)

This system allows electronic payments using the Internet, or telephone payments using voice response. After enrolling in the program, the taxpayers can login using their EIN or SSN, their PIN and a password. Payments can be made 24 hours a day / 7 days a week.

After enrolling in EFTPS either through the website or by phone at 1-800-555-4477, you can begin to make payments. To do this, you must provide three pieces of information: your SSN or EIN; a PIN, which will be provided to you in the mail; and an Internet password, which you select during enrollment.

Through EFPTS, you can make all federal tax payments, including for estimated taxes, excise taxes, income taxes and employment taxes. Payments can be scheduled up to 365 days in advance, and they can be canceled or altered up to two business days before they made.

- Debit or Credit Card

The IRS now accepts debit and major credit card payments through an approved third-party payment processor. These processors charge convenience charges that vary among the providers.

Each processor has its own processing fees, which are added to the balance owed. These fees are sometimes tax-deductible, so keep a record of your payments. The fee for using a credit card is usually between 1.88% - 2.35% for credit cards and $2.99 - $3.95 for debit cards. Since the types of cards accepted by the providers also vary, you, the taxpayer, may need to find the best provider for you.

Please keep in mind that you may be subject to credit card interest fees in excess of IRS non-payment fees, so if you can't pay your credit card balance in full, you could end up paying a lot more interest than you would have otherwise.

In order to use one of these services, you, the taxpayer, will need to provide all necessary Social Security Numbers (taxpayer and spouse if filing jointly), billing address, amount owed, credit card number/expiration/cvv, daytime telephone number and email address (used to confirm payment).

- Check or Money Order

Personal checks, cashier's checks and money orders are all accepted. When making payment this way, you, the taxpayer, will need to make sure to make it payable to the United States Treasury (rather than Internal Revenue Service or IRS). Include a daytime phone number, your SSN, note the tax year the payment is for and if the filing was a different-1040s.phpdifferent-1040s.phpdifferent-1040s.php, EZ, A and estimate payment. This should appear something like "XXX-XX-XXXX 2013 Form 1040EZ". Note: staples and paper clips should not be used to attach checks to vouchers.

Make your check or money order payable to the U.S. Treasury. Place it in the envelope with the form or notice loose; without clips or staples. If you are submitting a payment for your 1040, 1040A or 1040-EZ, complete and include Form 1040-V with your payment.

On the check or money order, include the following information:

- Your name, address and phone number

- Your social security number (SSN) or employer identification number (EIN)

- The applicable tax period

- The notice or form number that corresponds with your payment

- Pay with Direct Pay

The IRS lets taxpayers make payments directly from their checking and savings accounts through a feature called Direct Pay. You can make estimated monthly tax payments or pay your tax bill via this method.

Direct Pay is handled entirely online. The process is simple. After providing your tax information, you verify your identity by answering a series of questions. Next, you provide your personal information and then review and electronically sign the agreement. You will then receive a confirmation that you can print and/or save to your computer.

- Pay via Same Day Wire Transfer

If your tax payment is due imminently and there's no way to get it to the IRS on time to avoid fees and penalties, a wire transfer may be the fastest option. First, check with your financial institution to see if you can make wire transfers. Next, download and complete the Same-Day Taxpayer Worksheet and bring it to your bank. Please note that you must use a separate worksheet for each tax period and/or form.

IRS Payment Agreement

You may be eligible for an IRS payment plan if you owe $50,000 or less in individual income tax (including penalties and interest) as long as you up-to-date with your required tax returns. Businesses may be eligible for IRS installment agreements if they owe $25,000 or less in payroll taxes and if they have filed all of their required returns. If this is the case for you or your business, you can apply for an installment agreement with the with the IRS.

Remember, payment in full, can reduce (even eliminate) penalties, interest and help you avoid the fees associated with not paying your tax bill on time.

If you're unable to pay part or the entire amount of what you owe for any reason, make sure you first file your return in a timely manner. This should help you to avoid the failure-to-file penalty, which can be as much as 5 percent of the balance owed per month (up to a maximum of 25 percent). When you file on time without paying, penalties will still be assessed. However, those penalties are far less substantial, often 0.5 percent of the amount due per month in comparison.

After filling your return, the next step is to try and open up a line of communicate with the IRS to make a good faith effort to pay whatever you can. The following are some of the options that may be available to you if you are not prepared or able to pay your tax bill:

IRS Installment Plan

The IRS is often willing to grant IRS payment agreement (starting at just $25 a month), and applying for one can help you avoid more serious consequences like liens and levies. Installments accrue both interest and contain setup fees so it is not without cost.

To select this option, a person must first file their return and then complete an application for installment.

Applying for an Online IRS Installment AgreementIf you owe less than $50,000 in taxes, penalties and interest combined and have filed all of your returns, you may be eligible for an online payment agreement. It's especially likely if you have always filed and paid your taxes on time and owe less than $10,000.

Once you have transmitted all required tax returns including any prior year returns you can begin the process by applying online through the IRS website. You will need to create a user login, and to do this you must provide the following information:

- Full name

- Email address

- Address from most recent tax return

- Filing status

- Date of birth

- Social security number

To begin making installment payments to the IRS, you will need to complete Form 9465 - Installment Agreement Request (found here). You will also need to complete Form 433-F - Collection Information Statement (here).

Keep in mind that even if you are approved for an installment plan, interest fees and penalties keep accruing on the balance owed.

Typical fees for an installment plan is as follows:

- A one-time fee of $120 for the service

- Direct debit plan $52.

- Payroll deduction plan $105. Certain low-income individuals may qualify for a reduced fee of $43

Small businesses with employees may also be eligible to request an IRS installment agreement if they owe $25,000 or less at the time the agreement is established or if they are able to pay down any excess amount over the $25,000 that is due prior to entering into the agreement. Note that the IRS requires that small businesses enroll in a Direct Debit Installment Agreement if the amount owed is between $10,000 and $25,000. Businesses can apply online if they owe $25,000 or less in payroll taxes, or they can call the number on their bill or notice or the IRS Business and Specialty Tax assistance line (800-829-4933).

Even if you or your business are not eligible for an online IRS payment agreement, you can still make partial payments to the IRS which may help to lower interest expense. To initiate the process, call the phone number on your bill or notice. If no notice or bill is available, call 1-800-829-1040 for assistance.

Pay the IRS through an Offer in CompromiseIf you will be unable to settle your full tax liability and don't anticipate the ability to do so within three to five years, the IRS may be willing to accept a lump-sum offer. The agency refers to this as an Offer in Compromise (OIC), but only grants OICs under extreme circumstances.

You are not eligible for an OIC if you are not current with all of your filing requirements. If you are currently in active bankruptcy, OIC is also not an option. There are other eligibility requirements as well. To find out if you may qualify use the IRS's online Offer in Compromise Pre-Qualifier tool (you can find this here).

If it appears you are eligible for an OIC, you will need to file Form 656 - Offer in Compromise and Form 433-A - Collection Information Statement. An application of $186 applies. If you are applying for a periodic plan that stretches over 24 months, you must include your first payment when you file these forms. If you are opting for a lump-sum OIC, in which you pay a reduced bill in five payments or fewer and within five months of the IRS's acceptance, you must include a payment worth 20 percent of the reduced bill.

Circumstances that determine the compromise are as follows:

- The ability of the taxpayer to pay or not

- Current and projected income level

- Fixed expenses such as mortgage, rental payments, utilities and other liabilities

- Total assets and their related value

For questions regarding any of these options or information provided here, you may wish to contact the IRS for additional assistance. You can find contact information here.

While the IRS is often willing to work with taxpayers, please remember than they are legally bound to try and collect all of the taxes owed. If a taxpayer fails to make their required, under law, the IRS can place a lien against property, collect payment from wages paid by your employer, and freeze bank accounts as well as other legal remedies.